Types of Financial Statements

July 29, 2020

July 29, 2020  0 মন্তব্য

0 মন্তব্য

What are Types of Financial Statements?

The financial statements are critical reports as it describes the financial condition of a business. These are prepared by the management of the business to describe the financial position of the business for a uttered monetary age and can be universally classified as the income statement, sector balance sheets, cashflow accounts, and statement of owner’s equity.

Explanation

The financial statements of the business or an organization helps in sharing the financial position of the business to the creditors, investors, and specialists. They then shortlist broad-minded facets drawn from the financial statements and thereby derive meaningful presumptions. Such presumptions would then result in actions as planned by the stakeholders.

The financial statements can be universally classified as balance sheet, income evidence, cashflow proclamations, and statements of owner’s equity. These can be prepared on a quarterly basis, monthly basis, semi-annually basis, and on an annual basis. They are to be prepared as per the practice guidelines placed in the accounting principles as laid down by the regulatory power. In sit being words, they should be prepared in the standardized form so that such statements can be easily with the other financial statements of business that form part of the organization.

Generally, the balance sheet would describe the financial situation of the business as to how they stand in terms of assets and liabilities. The income word describes the profitability of the business and provide an explanation of the income series generated by the business. The cashflow announcement describes the exact cashflow orientation of the business that is how the inflows and outflows of cash happens in the business from the prior age to the current period.

Form of Financial Statements

The forms can be described as shared below: –

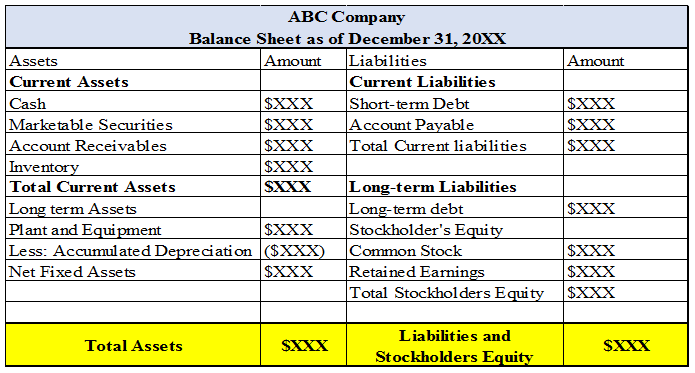

1. Balance Sheet

The balance sheet describes the financial position of the business and it extradites critical and important revelations on how the investments of the company or business are in place. Such information materials and penetrations “couldve been” both on discernible and intangible speculations and assets. The balance sheet also provides information pertaining to the debt and equity concoction. It can be described as the financial statements which is regarded as the final outcome resulting from on all financial statements.

The balance sheet is prepared expend the below equation 😛 TAGEND Total Resources= Drawbacks+ Shareholder’s Equity

The following can be regarded as the precedent of the balance sheet as displayed below 😛 TAGEND

At the resource section, there is the presence of money, marketable insurances, account receivables, Inventory, Plant properties, and Equipment. Generally, cash express the amount the business has on hand or it has placed in the current account. The marketable certificates can comprise of mutual funds, stocks and bonds which can be converted to cash within one to two business epoches. The chronicle receivables can be worded as the amount that the business owes from their clients when they sell items on credit. Inventoryings can be classified as the items that the business intend to sell.

Similarly, on the obligations segment, the business may regard short-term indebtedness such as short fraction or the current portion of long-term debt. The current segment of indebtednes can be described as the amount that the business has to service in the current financial period. The long-term debt can be described as the amount that the business has to retire over several fiscal period of its lifecycle. Similarly, it may comprise of account payable which are amount that the business is liable to pay to the suppliers from whom they have taken raw materials on credit.

2. Income Statements

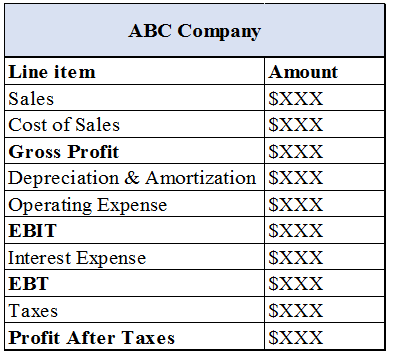

The balance sheet ordinarily prepared and presented is on as on time. It provides the overall snapshot of the liability’s situations, asset caste, and pay to equity mix. It is not describe the overall profitability that the business achieved and how they achieved their business proliferation. The income affirmation, hence, becomes important and it is the second statement that the investors sought to access so as to gain penetrations on the profit counts as shared by the income statements. Therefore, the income proclamation reports marketings, expenditures, benefits both before and after tax, and any losses that the business may incur. The operational expenses may comprise of Stipend, payment, dials, and internet, taxes, water statements, marketings and sell costs, taxes, stationaries, etc.

The following is the example of the income testimony 😛 TAGEND

Therefore, a general income statement comprises of auctions. From Sales, the cost of goods sold or costs of auctions is rebated to arrive at the gross profit. From the gross profit, operational expenses and depreciation are deducted to arrive at earnings before interest and taxes. From the earnings before interest and taxes, interest overhead is rebated to arrive at earnings before taxes. Ultimately, the taxes are withheld to arrive at the profit after taxes.

3. Cashflow Statements

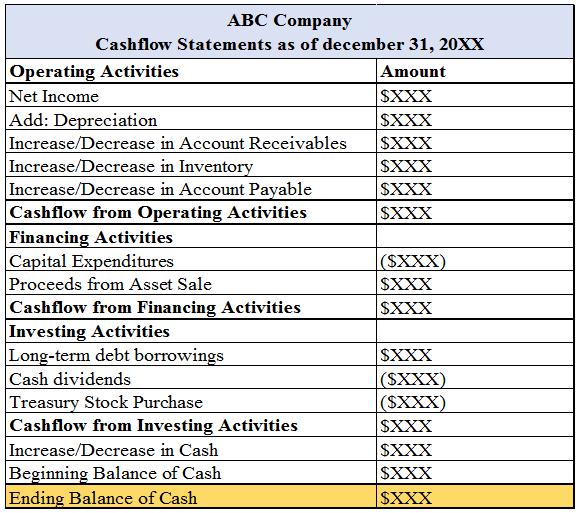

The statement of cashflows generally describe the overall cash outflow and cash inflow that the business knowledge during the financial period. This helps the investors and creditors ascertain that the business has enough to service its outlays and administer their purchases. The cashflow accounts are universally described in terms of operating cashflows, cashflows from financing activities, and cashflows from the investing activities.

The cashflow from business generally starts with the contributing up of non-cash expense into depreciation followed by the changes in assets and liabilities position. The cashflow from the funding works describes the changes in the cashflows growing due to retiring or elevating stores from obligation and equity as well as reporting of spreads and contributions. The cashflow from expending tasks describes the changes in the cashflows arising from purchase and sales of specified resources. The following is the example of cashflow testimonies as displayed below 😛 TAGEND

4. Statements of Equity

The statement of equity is of utmost importance to the existing as well as to the potential shareholders of the business. It mostly describes the changes that happen in the levels of retained earnings of the business. The computation of the net worth of the business is done by subtracting the debt of the business with the equity of the business.

Recommended Articles

This is a guide to Types of Financial Statements. Here we likewise discuss the above 4 different types of financial statements with item rationalization. You may also have a look at the following articles to learn more –

Users of Financial Statements Objectives of Financial Statements Limitations of Financial Statement Analysis Financial Reporting Examples

The post Types of Financial Statements saw first on EDUCBA.

Read more: educba.com